Yendo is a new secured credit card that uses your car as collateral and its value to determine your credit limit. And it's a useful tool for gig workers and individuals looking to leverage their vehicle to borrow.

But is Yendo legit? And is this credit card a good solution if you need quick money?

Our Yendo review is sharing how this card works, its requirements, and how to ultimately decide if it's right for you.

Want more fast money ideas besides Yendo? Checkout:

- EarnIn: Borrow up to $750 against an upcoming paycheck!

- Current: Earn 4% bonus and take out cash advances with this savings solution!

Key Takeaways:

- Cardholders can access $450 to $10,000 depending on the value of their car

- There’s no minimum credit score you need to apply

- Cards available for both owned and leased cars

- Cardholders must pay a $40 annual fee

- All cards subject to a 29.88% APR

Is Yendo Legit?

Yendo is legit and offers customers credit based on the value of their vehicle and their ability to pay. Cardholders put up their car as collateral which guarantees payment, and Yendo reserves the right to collect on this and if needed, repossess the vehicle.

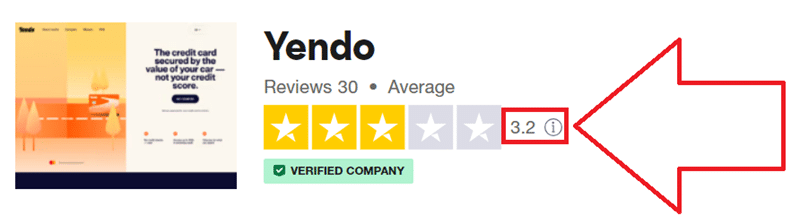

The company currently has an average rating of 3.2 stars on Trustpilot. Many positive reviews enjoy Yendo's high credit limit and the fact that it also offers cash advances. However, some negative reviews come from users who don't qualify for Yendo.

Depending on the individual and the value of the vehicle, Yendo offers consumers a credit limit up to $10,000. It’s worth noting that no one is ever guaranteed to qualify for this amount and each applicant will be evaluated individually.

How To Get $1,000 In 24 Hours.

What Is Yendo & What Does It Offer?

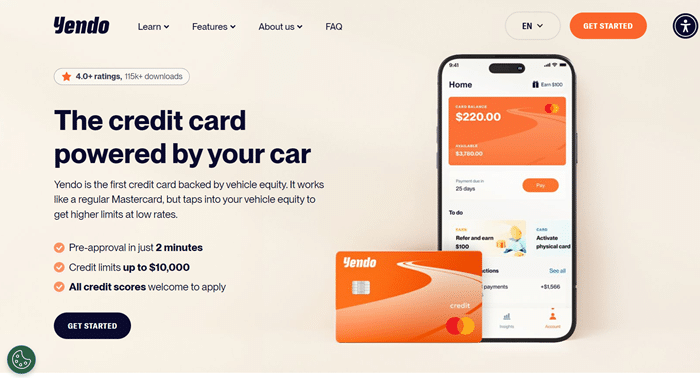

Yendo is a secured credit card company that began in 2021. The company lets vehicle owners use their cars as collateral to secure their credit limit, which is pretty innovative.

Unsecured credit cards let consumers access credit without having to put down any kind of security deposit or collateral. A secured credit card, on the other hand, requires the card holder to put up some kind of collateral that helps guarantee their payment. If for some reason the cardholder can’t make their payments, they would then have to forfeit this collateral.

According to Yendo, all credit scores can apply. Pre-approval only takes 2 minutes too. If you need quick money and find that a traditional secured credit card doesn't provide the limits you need, Yendo could be a viable alternative.

This review will focus on how Yendo's credit card works. But the company also offers several other services which I'll cover below as well.

Yendo Credit Card

The Yendo credit card is a secured Mastercard that’s available to consumers who either own or lease their car and have enough value in it to be used as collateral.

Applicants go through an approval process where your credit and income are checked and your vehicle’s title and value verified. Once approved, you receive notification of your credit limit, which ranges from $450 to $10,000.

There's some slight differences in the application process if you own your car or if you're still making payments. You either transfer your auto loan or your title to Yendo. Yendo then becomes a lienholder on the title, but ownership remains the same.

After that step, you gain access to a virtual Yendo card. You also receive a physical card in the mail. You can use your card anywhere that accepts Mastercard, and making on-time payments helps you build your credit score.

Your first payment is due 25 days after your first statement. You must pay 1% of the current balance or $50, whichever is higher. The Yendo card also charges 29.88% APR and has a $40 annual fee, so keep this in mind.

Also note: pre-approval doesn't impact your credit score. But going through with the full approval process will involve a credit pull, which can impact your score.

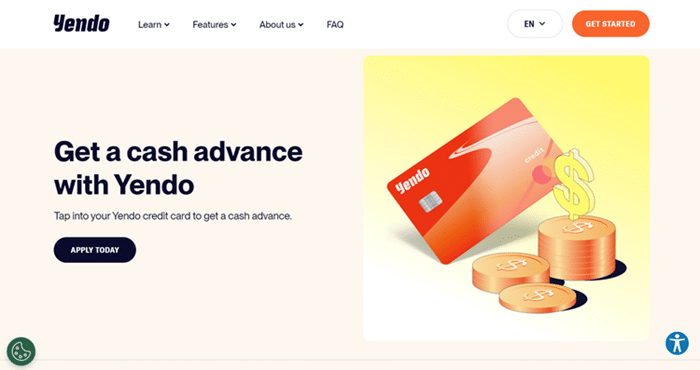

Cash Advances

Yendo cardholders can also use their account for cash advances. To use this service, you can use your card at any ATM and withdraw up to $400 a day, though the maximum amount you can receive in total can be no higher than 50% of your credit limit.

If you need money to pay rent tomorrow or other urgent bills, this feature is quite useful. And it certainly beats turning to solutions like payday loans.

However, Yendo charges a 3% fee for this service. You might also face additional fees issued by the ATM.

For this reason, the The Budget Diet team prefers apps like EarnIn, which offers up to $750 in a given pay period and doesn't charge expensive mandatory fees. You can also try Cleo if you're a gig worker or Dave or Super.com for more options.

Credit Building

Yendo reports your monthly payments to all three major credit agencies – Equifax, Experian, and TransUnion. If you have several successive on-time payments, it has the potential to improve your credit score.

However, this is likely more beneficial for those who have very little credit history to start with or have a very low score. Cardholders who already have a good credit score or an established credit history may not see any improvement, and in some cases may see a dip in their score. Additionally, if you fail to make on time payments, this too will be reported to the credit agencies and will eventually lower your score.

Pro Tip: Get your credit score report and ongoing monitoring from CheckFreeScore! This is an easy and comprehensive way to know your score and make a gameplan to improve it.

Auto Loan Refinancing

Yendo accepts members who don't own their vehicles and are still making loan payments. And during the application process, you can potentially transfer your loan to Yendo and refinance it along the way.

Yendo claims that the average cardholder lowers their monthly auto payment by $450. This is a pretty massive claim, and it's “based on the average monthly payment savings when comparing prior auto loan payment to new Yendo auto loan payment, with a 36-month repayment period.”

I'm not sure what Yendo customer loans look like on average, but $450 in extra savings per month is pretty massive. But again, not everyone qualifies for a Yendo card. And if you have an existing auto loan, you'll likely get a much lower Yendo credit limit that you slowly increase over time as you pay down your loan balance.

Referral Program

Current Yendo cardholders can recommend friends or family to the service by using the referral program.

After logging into your account through the Yendo app, you simply click on the “Get $100” button and you’ll see a referral link that you can then share with friends. If your friend is then approved for and signs up for a card, you will receive a $100 credit on your statement.

Our post on the best referral bonus apps has even more opportunities to snag free money if you're interested.

Yendo Credit Card Requirements

There are a few basic requirements to qualify for the Yendo credit card, including:

- Being at least 18 years old

- Owning or leasing your car

- Having a vehicle that was made in 1996 or later

- Having a valid email address and smartphone

- Having a Social Security Number or taxpayer ID number

- Living in one of the following states: Alabama, Arizona, Arkansas, California, Colorado, Connecticut, Delaware, Florida, Georgia, Idaho, Illinois, Indiana, Kansas, Kentucky, Michigan, Mississippi, Montana, Nebraska, Nevada, New Hampshire, New Jersey, New Mexico, North Carolina, North Dakota, Ohio, Oregon, Pennsylvania, Rhode Island, South Carolina, Tennessee, Texas, Utah, Vermont, Virginia, Washington, West Virginia, or Wyoming.

- Having an “income that can support your monthly obligations” (there’s no specific information on what the minimum income level an applicant needs)

Again, you can go through pre-approval without impacting your credit score. But not every applicant is approved, and your credit limit ranges from $450 to $10,000.

Yendo Fees & Pricing

Yendo cardholders must pay a $40 annual fee in addition to making minimum payments on their balance. Any remaining balance that’s carried over each month will accrue interest at a 29.88% annual percentage rate (APR).

If you pay off your balance in full each month, you don't have to make any interest payments and the only fee you’ll be responsible for is the $40 annual charge.

Is Yendo A Title Loan? – How Your Credit Limit Works

No. Although a title loan works in a similar manner to Yendo’s credit card, they're not the same thing.

A title loan also allows you to access a line of credit or a short term loan based on the value of your car, but the terms usually require you to pay this back in full after about 30 days. Title loans are also only available to those who own their cars outright and are not an option for those who lease. Plus, title loans tend to have higher upfront fees than Yendo.

Both title loans and the Yendo credit card establish your credit limit or loan amount based on the valuation of your car, but Yendo also considers your income level. Lastly, Yendo allows its cardholders to pay back their balance over time.

The Best Instant $25 Sign Up Bonuses.

What Happens If You Don’t Pay Yendo Back?

For cardholders who aren’t able to make payments on their balance for whatever reason, Yendo claims it can help. So, if you’re unable to make your minimum payment, or if you’re having trouble meeting your payment obligations altogether, you should first stop using your card, and then reach out to Yendo.

Yendo advises all its cardholders to contact its customer service team right away if they find they’re unable to make their minimum payment to work towards a solution. Although Yendo does retain the right to repossess your car due to nonpayment, it says this is their last option. It should be noted that any lien holder can use this as leverage to collect on outstanding payments which could mean losing your car.

Other Yendo Credit Card Reviews

Yendo receives mixed reviews from its customers. Positive reviews include comments on how easy the application process was and how fast they were able to use their new card and access cash. Negative reviews comment on deceptive advertising tactics and quoting initial credit limits that were much higher than they actually got when the approval process was complete.

Here are a few Yendo reviews we found on Trustpilot or social media for some examples:

“I just wanted to share my experience with Yenndo and how it's been a great opportunity for me to build some credit, as well as pay some bills that were coming up at an untimely event” – Jason T. Springfield, OR, Yendo review.

“It was an easy process and had access to funds immediately. Can make payments to keep open as needed. Would use again in a minute!” Customer review, Trustpilot.

“Saw an ad on YT and it literally says no credit check but yet they do check your credit so that's a lie to get you to their website. Then their site says that the credit check won't affect your credit which is also a lie as they do a hard inquiry not a soft credit check like Capital One. Very deceptive so I will not get credit with them as they have shady business practices off jump.” J W, Trustpilot.

Again, it's important to remember that while pre-approval doesn't impact your credit score, the full approval process can. And most cardholders won't qualify for the full $10,000 limit.

Pros & Cons

Pros:

- Easy application process

- Provides up to $10,000 in a credit limit

- Yendo also offers cash advances

- Yendo works with vehicle owners and leasers

- Pre-approval doesn't impact your credit score

Cons:

- Yendo has a $40 annual fee

- Many customers don't qualify for a high credit limit

- High cash advance fees

- Yendo isn't available in every state

Is There Customer Service?

If you’re interested in learning more about Yendo or are a current cardholder, you can contact the company by emailing [email protected] or calling (888) 532-0770. You can also issue a complaint at [email protected].

Is Yendo Worth It?

Yendo is worth it for vehicle owners who want an alternative lending option that's available to all credit scores. And if you have a stable income and can make on-time payments, its card could be right for you.

However, any credit card requires responsible usage. If you have inconsistent income or aren't good at making on-time payments, Yendo probably isn’t the best choice because you’ll build up a lot of interest and may risk losing your car altogether.

Ultimately, we like that Yendo provides an innovative opportunity for vehicle owners and leasers. If you make money with Uber Eats or DoorDash or just want to use your vehicle to borrow money against, Yendo could be the solution you're looking for.

Want even more money-making ideas? Checkout:

- The Best Apps To Earn $100 A Day.

- Is Klover Legit & Worth It? Borrow Up To $200.

- The 20+ Best Free Apps Paying Instantly.

Yendo Review

Name: Yendo

Description: Yendo is a secured credit card that lets cardholders access $450 to $10,000 in a credit limit based on the value of their car.

Operating System: Desktop, Android, iOS

Application Category: Credit Cards

Author: Tom Blake

-

Credit Limit

-

Application Process

-

Fees

-

Other Perks